- Introduction

- Models Of Digital Governance

- Broadcasting / Wider Dissemination Model,

- Critical Flow Model

- Comparative Analysis Model

- Mobilization And Lobbying Model

- Interactive – Service Model / Government-To-Citizen-To-Government Model (G2c2g)

- E-Government Maturity Model

- Five Maturity Level

- Characteristics Of Maturity Model

- Towards Good Governance Through E-Governance Models

- Practice Questions

- Network Infrastructure

- Computing Infrastructure

- Data Centers

- E-Government Architecture

- Interoperability Framework

- Cloud Governance

- E-Readiness

- Data System Infrastructure

- Legal Infrastructural Preparedness

- Institutional Infrastructural Preparedness

- Human Infrastructural Preparedness

- Technological Infrastructural Preparedness

- E-Government Initiatives In Nepal

- Cyber Laws

- Implementation In The Land Reform

- Human Resource Management Software

- Nicnet

- Collectorate

- Collectorate

- Computer-Aided Administration Of Registration Department (Card)

- Smart Nagarpalika

- National Reservoir Level And Capacity Monitoring System

- Computerization In Andra Pradesh

- Ekal Seva Kendra

- Sachivalaya Vahini

- Bhoomi

- It In Judiciary

- E-Khazana

- Dgft

- Praja

- E-Seva

- E- Panchyat

- General Information Services Of National Informatics

- Centre E-Governance Initiative In Usa

- E-Governance In China

- E-Governance In Brazil And Sri Lanka

Introduction

In tune with the policy initiative taken up by the Government of Andhra Pradesh for effective utilization of Information Technology as part of e-Governance project, National Informatics Centre, Hyderabad has taken up online computerization for the its Districts Treasury (DTO), Sub Treasury (STO) and Pay and Accounts Offices (PAO) Offices in 330 locations across the state.

E-Khazana is an online application that takes care of entry level validation and budget control and pre-audit rules at Auditor level and finally for issue of cheque/pass order at passing level. After reconciliation with bank, monthly accounts will be generated for submission to Accountant General.

The Administrators' role is very important in this application as be will be responsible for

- Assigning the roles.

- Watching budget expenditure.

- Head of accounts, and

- Drawing and disbursing officer.

It is an intranet applications that works on linux/Windows platform with backend as postages SQL 7.3 and front-end is PHP 4.1 (Hypertext Pre Processor).

The Treasury System in AP

Director of Treasury and Accounts (DTA) is the administrative head of treasuries and accounts department.

STO office is responsible for compiling all the payments through DDOs and receipts through challans. This data is sent to DTO on a daily basis. They also send Pensioner details and Class IV GPF details to DTO on a monthly basis. There are around 300 STO offices at the sub-district level in the State.

DTOs in turn compile all the accounts (Payments and Receipts) processed through its associated Sub Treasury Office (STO) and are located at the District headquarters. They are also responsible for sending reports to AG office and DTA. DTO offices in the state are located at 23 District Headquarters.

Office of the Directorate of Treasury and Accounts (DTA) is responsible for compilation of all Payments and Receipts processed through DTO (District Treasury Office) on daily basis and sending sports to Finance dept. (Budget section), CM's office, and to other Heads of Department (HoDs).

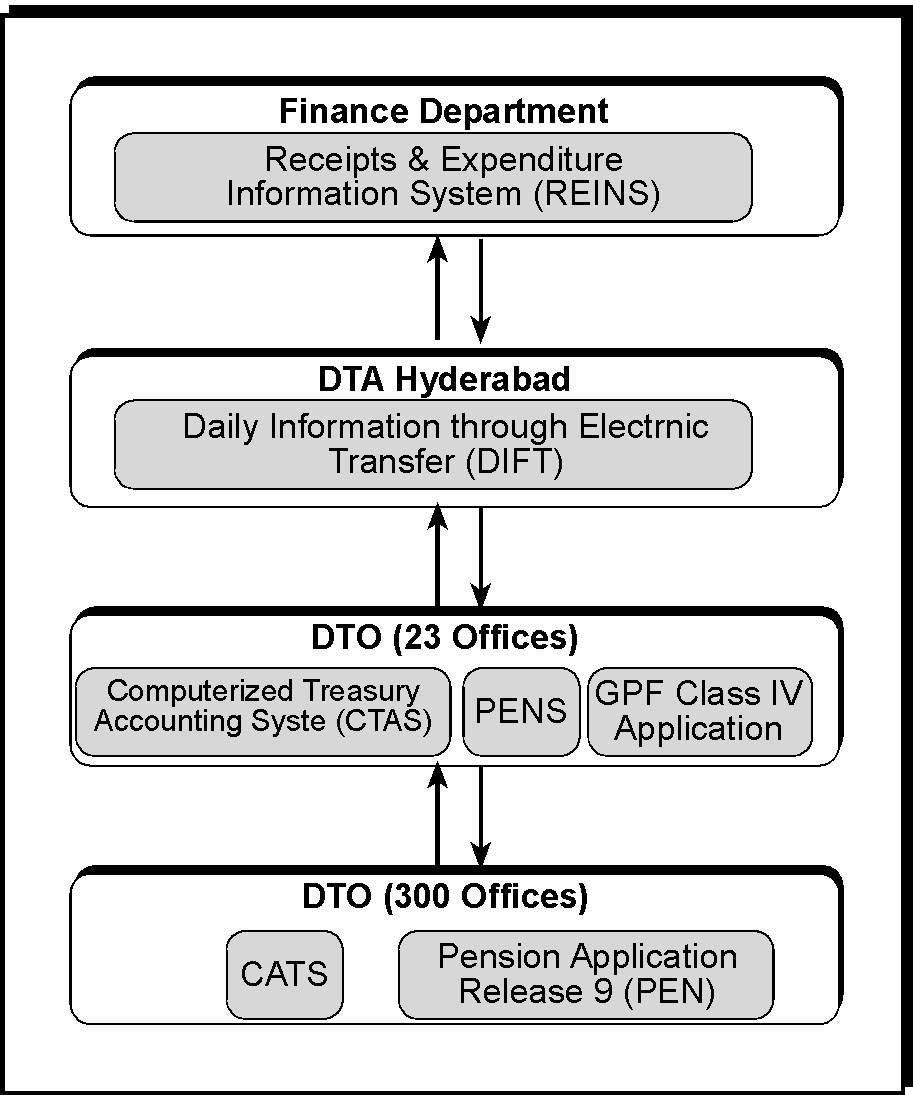

Figure 5.2.11.1 shows the hierarchy of offices in the Treasuries Department, in the Government of AP.

Figure: Hierarchy of offices in Treasuries Department

Introduction to Functions of Treasury

Functions of the Treasury are broadly classified as:

- Treasury functions

- Accounts functions

Treasury functions

These functions can be summarized as follow:

- Receipts and payments made either by cash (bills or cheques) adjustments (bills or cheques)

- Conducting Government's financial transactions such as payment of salaries, other payments like TA, LTC, cont5iagent rents, loans and advance, receipts of Government revenue, etc.

- Conducting or cash transactions through non-banking treasuries and banks.

- Payment of pensions

- Pre-audit of bills and post-audit of vouchers

- Reconciliation of the valuable articles such as election boxes, examinations papers, department cash chest treasuries trove, and the like.

- Receipt, safe custody and sale of various kinds of stamps.

- Payments of Government Securities such as Stock certificates, bearer bonds, promissory notes and income tax deductions

- Exercise treasury control over all departmental financial transactions with reference to Budget.

- Maintenance of GDF account of last grade employees

- Maintenance of Employees Welfare Fund Account of employees

- Regulation of appointment to the public service through Act-2 of 1994.

- Rendering of daily figures of Finance department

- Rendering of classified accounts to the AG

- Maintenance of deposit accounts including GO No. 43.

- Maintenance of User charges Accounts.

- Submission of PMES information to Government

- Enforcing accountability on DDOs and reporting to the Government as per GO NO. 507.

- Maintenance of employee census database.

Accounting functions

Accounting functions include the following:

- Rendering financial advice to head of the department

- Preparation of budget estimates of the respective departments.

- Maintenance of departmental accounts in the respective departments

- Reconciliations of the receipts and expenditure of the department

- Processing of the pension cases of the respective departments

- Internal audit of the Department Unit Offices and follow-up action for settlement of the audit objections.

Reports generated by treasuries and accounts department

- Classified Accounts to AG-STO/DTO level

- GO No. 507–STO/DTO/RJD/DTA/PPO/APPO

- PMES-STODTO/RJD/DTA/PPO/APPO

- Daily figures-STO/DTO/DTA

- Receipts and Payment Reconciliation-DDO-HOA wise

- Pensions/strong room stamps

- Budget vs. Expenditure –DDO wise and object headwise

- Non-Banking Sub treasuries

- Class IV GPF/EWF

- Deposits Accounts and GO No. 43

- User Charges

- Employee Census

- Any other report required with available data.

System Overview

Budget authorization

The DTA, after exercising check on Distribution Statements furnished by HoD's with reference to Budget Releasing Orders (BRO) and Budget Estimates (BE) approved by the Assembly, issues authorizations to the DTO's concerned for Budget distribution made by the HoD.

Redistribution/Reauthorization

At any District, the subordinate controlling officer or the Head of the District, further distributes the Budget down the line to each Drawing officer and sends a copy of this budget distribution statement to the DTO. The DTO, after exercising proper cheques with reference to the Budget authorized by the DTA, issue, re-authorization to the STO concerned.

The Treasury Officer permits the Drawing and Disbursing Officer (DDO) to draw the money to the extent of authorized Budget provision.

Honouring of Claims against government

The DDO from each offices office presents their claims to the Treasury department for withdrawn of money for various purpose like "Payment of salaries, implementation of various schemes, meeting of day-to-day expenditures in the officers, etc." Based on the nature of the claim, different bill forms are used.

Treasuries honour these claims after scrutinizing the admissibility of the claim, financial powers of the drawing officer, sanction orders required, the genuineness of the claim, etc. besides availability of budget. After thorough examination of the claim presented by the DDOs, the Bill is passed or the Bill is returned when it is not in order duly quoting the authority for its return.

Acceptance of receipts

Receipts that accrue to the Exchequer are remitted through an instrument called challan. This challan form is used for all sorts of receipts like tax revenue or fees to be paid or a recovery.

Treasury checks the challan whether HoA is reflected on the challan with reference to the purpose of remittance and the Department on whose behalf the remittance is made. An entry is made in a register and serial number of the entry is noted down on the challan with date. The Treasury officer in token of having checked the same appends stamped signature on challan and then only the challan is accepted in the Bank for remittance.

Verification and certification of bank scrolls

Bank scrolls received together with the paid vouchers, cheques, or challans, are verified on a daily and monthly basis, RBDs are arrived at and certified before finalization of the daily/monthly accounts by the treasuries.

Rendering of daily and monthly accounts

For any receipts and payments for the day, every bank branch sends both challan's and the paid voucher's list to the concerned treasury. Each day, STO sends statements of receipts and payments to the DTO, who takes into accounts the receipts and payments in the District and Accounts rendered by its sub-offices. DTO prepares daily accounts and submits to the DTA. DTA in turn furnishes the consolidated daily figures to the Government.

All sub-treasuries, at the closure of the month, daily accounts for the months are classified into sub-accounts as required by the AG's and the same are furnished to the DTO. Treasury at District consolidates them as Sub-Accounts and Main Account and Furnishes to the AG on or before the specified due date.

HoA-wise figure are submitted to the DTA, who in turn submits consolidated figures to the Finance Department Consolidation and rendering of daily/monthly accounts are handled using software package called C-TAS (Computerized Treasury Accounting System) and DIET (Daily Information through Electronic Transfer) which were developed in-house.

Supply of Stamps to Sub-registrars in Districts

Treasuries undertake another important revenue earning function of the State Government. The Treasury, as a Local Deposit, stores the Non-Judicial and Judicial Stamps required for registration and other purposes.

Treasuries keep sufficient stocks of stamps by placing by placing timely indents to the Inspector General of Registration and Stamps, and supply the same to the Stamp Vendors and to the Sub-Registrars. They render Plus/Minus Accounts every months to the AG and to the Inspector General of Registration and Stamps. Treasury Officer conducts annual stock inspection of stamps held by Sub-Treasuries and the Sub-Registrars.

Preparation of budget estimates

The Department prepares Budget Estimates, by collecting Number statement and other estimates from all the District Units. It submits the same to the Finance Department duly taking int accounts the Budget estimates and revised estimates of the previous year, the expenditure estimated under various heads for the current financial year strictly adhering to the norms prescribed.

Context Diagrams

The context diagram for Treasuries is depicted here as Figure C11.2 to show the system level context diagrams.

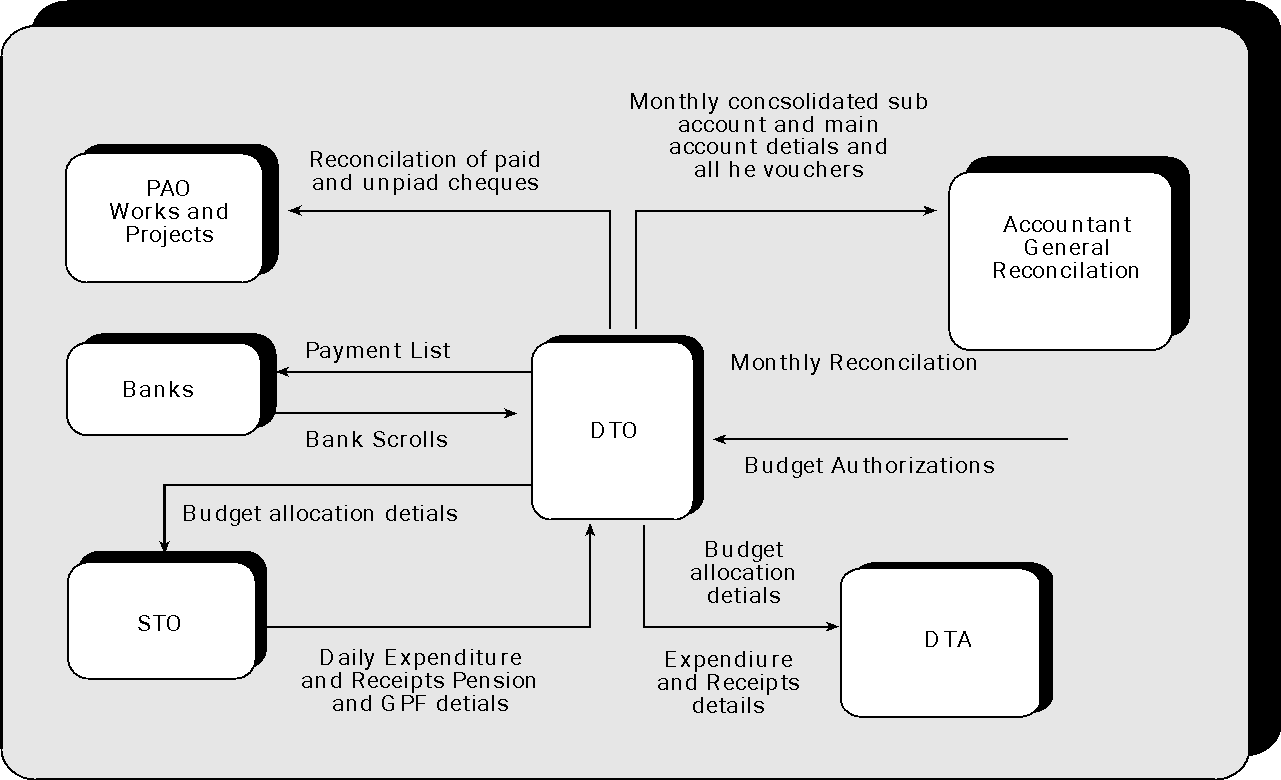

Overview of District Treasury Office Functions

Figure presents an overview of the DTO functions:

Figure: District Treasury Office Functions

Core Functions of POA–Twin Cities

Let us summarize the core functions of payment and Allowance Office (PAO) in the twin cities of Hyderabad and Secundarabad:

- Payment of regular pay and allowance

- Regulation of pay and allowance of AIS officers.

- Maintenance of GIS of AIS officers.

- Regulation of Leave Salary and pension contribution for AIS officers who are on foreign service.

- Maintenance of Class-IV GPF accounts.

- Reconciliation of paid cheques.

- Preparation of Civil list of AIS officers during January and July.

- Payment of salaries through Electronic clearing system to the Honourable ministers, Hon'bnle High Court Judges, Senior officers in secretariat and Gazetted Officers, Heads of Departments and all Government employees in the Twin Cities.

- Rendering of Accounts to Accountant General/Finance Department Pre-audit of claims

- Monitoring the submission of the DC Bills for the AC Bills drawn

- Submission of PMES Information to Government

- Enforcing accountability on DDOs and reporting to the Government as Per GO NO. 507.

- Maintenance of employee census database.

Budget Allocation from Finance Department

Subordinates of each department (DDOs) send budget proposal regarding their needs to their respective Head of the Department. HoDs of each department verify and send it to their concerned department in Secretariat which in turn submit the proposal to the Finance Department.

On receiving the proposals, the Finance Department allocates the Budget and sends the Budget Allotment information to the HoDs of each department. On receiving the Budget allotment information. HoDs of each department prepare Redistribution of Budget Information for their subordinates and will send one copy of Redistribution of Budget Information to their Subordinates (DDOs) and there copies to DTA. ADA Keeps one of the three copies with itself. DTA sends the second copy to the Audit Officer (DTO for districts and PAO for Twin Cities) DTA sends the third copy (Authorized and Stamped) to the Subordinates (DDOs).

Scrutiny of Bills and Approval by PAO

The DDO of the concerned department submits the bill of government expenditure at the PAO and receives a token as an acknowledgement. The validity of the bill is checked as per the government rules for the specimen signature and arithmetic accuracy, in the three states Ay Auditor, Superintendent, APAO/"Deputy PAO at PAO. If the bill satisfies the stipulated regulations, a pay order will be issued. If it doesn't, it is considered as a rejected order (the same process is executed by the superintended APAO/Deputy PAO).

If the bill is passed, it will be approved by the approving authority, APAO (Assistant Pay and Accounts Officer) Deputy PAO. If the bill amount exceeds Rs. 5 Lakhs and up to 1 crore, PAO's approval is necessary. Bills related to arrears will be sent to the APAO/Deputy PAO. Bills related to Electricity, Water, Telephones, etc will approved by the Superintendent.

After the approval of any bill, it goes to the cheque writing section and then goes to the cheque delivery counter. The DDO or its representative can collect the cheque from the cheque, Delivery Counter.

Based on the nature of claim, PAO issues payment in following manner:

a. In case of corporations, PAO sends a Letter of Credit (LoC) to the Corporation (e.g. Government Funds allotment).

b. In case of DDOs, PAO issues cheque for the total amount on the name of Bank Manager, SBH and list of DDOs. The Bank manager credits amount to respective DDOs.

c. In case of the individual having account in any bank the cheque on total amount will be sent to Bank Manager, SBH and the list is sent to RBI as well. Banks in turn credit amount to invidiual accounts.

d. In case of any firm, which has supplied the material (e.g. computer hardware) to the concerned government departments, PAO issues a cheque on the firm name but the cheque will be sent to the concerned DDO.

PAO maintains the list of payments done on that particular day and will assign a number against each issued cheque. This number is called voucher number. From then onwards the voucher references the bill number. All the vouchers are sent to the computer section for data entry. Reports are generated Daily/Monthly and are sent to different departments.

Functions of E-Khazana

National Informatics Centre, Hyderabad has developed Treasury application e-Khazana, " an advanced, integrated software package with the following features:

Outline of the Functions of E-Khazana

The functions of e-Khazana are:

- Token issuing

- Budget verification and monitoring.

- DDO/HOA access verification

- Bill auditing

- Bill process log for entre bill life cycle.

- Pay order generation

- Bank list processing

- Bill status

- Reconciliation with bank scroll

- Daily and monthly reports generation

- Reports on Receipt and expenditure Status at any point of time.

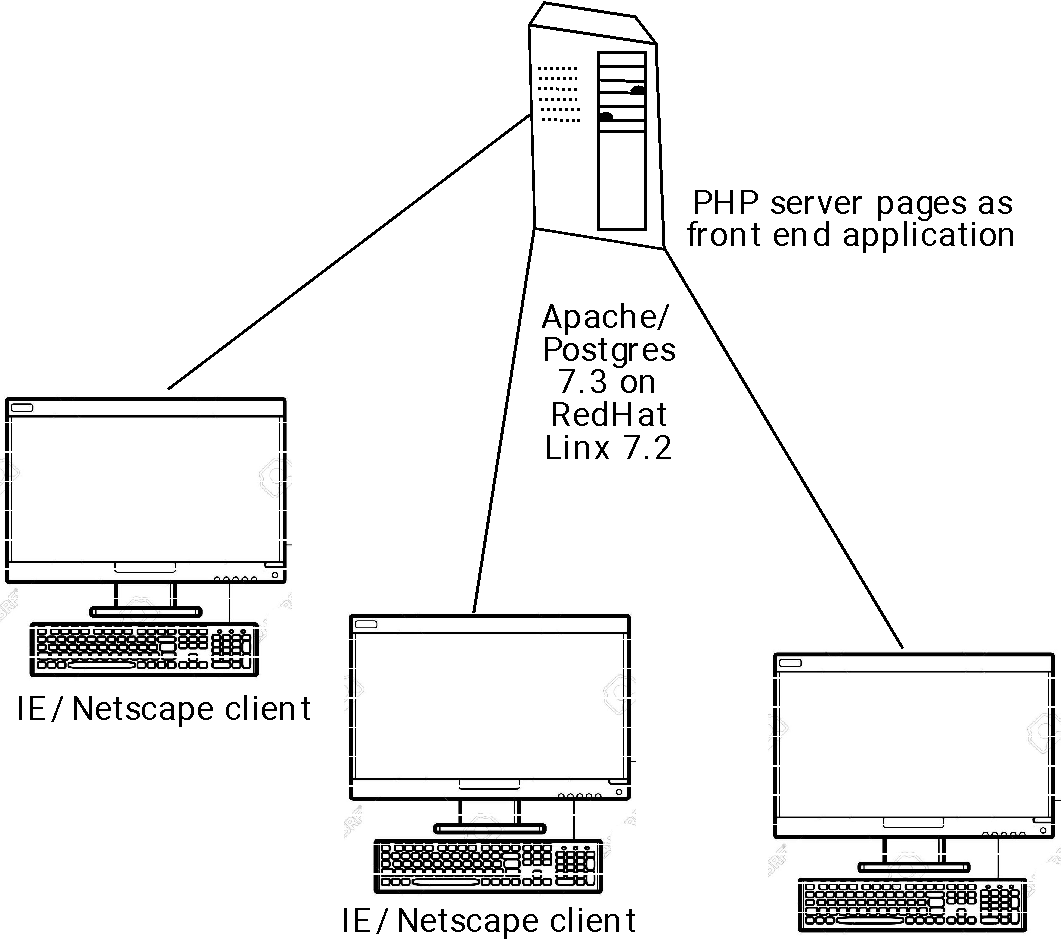

Outline of E-Khazana System Architecture

Figure gives a brief outline of the e-khazana system architecture.

Figure: Illustration of E-Khazana architecture.

Application architecture

It is a 3-tire architecture. Application is built using Hyper Text Pre-processor server pages, HTML and JavaScript. Back-end in postages SQL 7.3.

Automatic of functionality

It is a workflow automation tool used for disbursing and accepting funds to various government originations after auditing the application and documenters for meeting the requirements. The workflow starts with issuing of a transactions ID. Budget and other master data are maintained separately. Check list for each kind of transactions is also maintained as part of master data.

Application flow

Figure illustrates the application flow.

- SLO: (Substantiative Level and Officer) process is to maintain cadre strength designation–wise. It should match with the bill submitted by the DDO.

- Accounts: Process is for generating monthly accounts for submission to Account General.